Cook for yourself instead of eating out.

Preparing your own meals can save 20% or more on food costs. There’s no way around it—eating at a restaurant or getting takeout is much more expensive than making a meal at home. If you’re looking to cut your monthly spending, eat out sparingly and prepare most of your meals at home. Pack your lunch instead of buying food at work or school. To save time, cook multiple meals at once and put them in the fridge or freezer to reheat later. Preparing your own meals is not only cheaper, it’s nearly always healthier as well. Healthy home-cooked foods like veggies, beans, and whole grains are cheaper and more filling than fast food or prepackaged snacks.

Bring beverages from home instead of buying them.

Carry your own water bottle or coffee thermos to save money. Spending $1 or $2 on bottled water, or twice that much on a cup of coffee, may not seem like much. But that can quickly add up to $20 USD or more per week. Instead, fill up your own reusable water bottle in the morning and refill it as needed throughout the day. If you’re a coffee drinker, invest in a coffee pot and a thermos to make your own coffee and bring it with you to work or school. Whatever kind of drink you prefer—from iced tea to smoothies to bottled sodas—it’s cheaper to bring your own from home instead of buying it at a shop or vending machine while you’re out. If you like flavored coffee, buy syrups and flavored creamers to make your coffee taste the way you like it.

Shop with a grocery list and stick to it.

Always make a shopping list before you go to the store. The list gives you a clear idea of what you need and eliminates unnecessary purchases—but only if you focus on getting just what’s on the list! Take a look around your kitchen to determine what you need before you go to the store, and do your best to stick to your list as you shop. If you go “off-list,” do it because a similar item is on sale—for instance, buying apples instead of pears because they’re a better deal. Fight the urge to make unnecessary impulse buys.

Check for sales and use coupons.

Take advantage of ways to save money on the grocery items you need. While making up your shopping list, go through store flyers and browse the internet for coupons and special deals. Don’t buy items you don’t really need just because you have coupons for them, but do make sure you use every cost-saving measure out there for the items you do need. For example: Buy non-perishable items in bulk when they’re on sale, so long as you have room for them and know you’ll use them up over time. Buy fresh foods that are in season. They will cost less than the fresh food flown in from the other side of the world. Buy generics that are equivalent to name-brand items.

Identify needs, wants, and unnecessary items when shopping.

Stop and ask yourself how important it is to spend on something. If the expenditure is a necessity, like buying a new laptop for work or school, definitely do it (but hunt for the best deal). If it’s a want, like a new shirt, consider if your money would be better spent (or saved) elsewhere. If it’s an unnecessary expenditure, like buying a cool pair of shoes when you have a very similar pair sitting at home, avoid it!

Cut back on or quit vices like smoking.

It’s not easy to stop buying tobacco or alcohol, but you can save big. Quitting smoking is not only great for your health, it’s also a great way to reduce expenses—if you smoke a pack a day, you’ll save around $2,000 USD per year by quitting. Cutting back on or cutting out alcohol is also a healthy choice that can save you money—the average American adult spends $1,200 USD per year on beer alone. Unless you’re both really skilled and exceptionally lucky all the time, quitting gambling will also save you money.

Pay with cash when you’re shopping.

It’s harder psychologically to part with cash versus swiping a card. When you pull that cash out of your wallet and take a look at it, you’re more aware of its value and what you’re giving up to make a purchase. You just don’t get the same psychological impact from using a credit card, debit card, smartphone app, or even paper check for that matter. Shopping only with cash also makes it easier to stick to your budget—if your wallet is empty, you have to be done shopping! If you’re already carrying a high-interest balance on your credit card, spending with cash will definitely save you money, even if you buy the exact same stuff. Better yet, though, don’t spend the cash and use it to pay down your credit card debt.

Pay off high-rate credit card debts.

Prioritize high-interest debt reduction for long-term benefits. Investing money in your savings is often the better option than paying off low-interest debts, but credit cards nearly always carry sky-high interest rates. Direct as much of your budget as you can manage toward paying off high-interest credit cards—you may not see immediate budget savings, but within maybe 6 months, or a year, or a couple of years, you will. And the budget benefits will only grow in the longer term.

Set your phone to use Wi-Fi whenever possible.

Make sure you’re not wasting money on cellular data usage. Check your smartphone’s settings to make sure it automatically uses Wi-Fi for data whenever it’s available. Reducing your monthly cellular data usage means you can switch to a lower-cost data plan, which can easily save you $20 USD or more per month. Instead of paying for a set amount of cellular data per month, see if your wireless provider offers a “by the gig” plan that charges you based more closely on the amount of data you actually use. In some—but not all—cases this type of plan may save you money.

Cut your cable TV or landline phone.

Don’t waste money when you already pay for viable alternatives. With all the streaming options out there, you may be able to “cut the cord” and save over $100 USD per month without much impact on your entertainment options. But make sure you’re actually using the streaming services you subscribe to as well—you might save another $20 or $30 USD per month by cutting back on those. If you still have a landline phone, cancel your service and rely on your cell phone.

Cancel unnecessary memberships and subscriptions.

Cutting out cable TV is a good start, but don’t stop there. Evaluate other subscriptions as well—things like gym memberships, food delivery services, and so on. Keep them only if you’re absolutely sure you’re getting your money’s worth, and even then consider canceling them temporarily until you get your finances in order. At the very least, call the provider and say you’re planning to cancel—you’ll be surprised how often they’ll be willing to renegotiate! Subscriptions and memberships are often automatically charged to your credit card or bank account, so check your statements to make sure you’re not still paying for subscriptions you forgot all about.

Renegotiate your rent or house payment.

Work with your landlord or mortgage lender to cut your costs. Changing tenants can be a hassle for landlords, so they may be willing to reduce your rent a little if you say you plan on moving otherwise. Don’t expect miraculous reductions, especially in a hot rental market, but maybe you can save yourself $25 or $50 USD per month this way. If you own your home, contact your mortgage lender and several competitors to evaluate the rates and costs for refinancing your mortgage. If you refinance at the right time and the right interest rate, this can be a path to hundreds of dollars in savings per month.

Downsize your current living arrangement.

Find a cheaper place, get a roommate, or move in with your parents. If you can’t reduce your current rent or mortgage payment but still want to live on your own, start looking for a cheaper place to live that’s acceptable (instead of ideal) for your needs. Alternatively, bite the bullet and look for one or more roommates to share housing payments with, but make sure you do your homework and choose the right roommates. Finding a roommate can save you a good amount of money per month, but moving back in with your parents can save you even more. To make it a bit easier to swallow your pride, pay your parents a nominal amount of rent and take care of your own stuff (like laundry).

Bundle your home and auto insurance.

Bundling your policies often results in savings of up to 25%. If you have auto insurance and either renter’s or homeowner’s insurance with separate companies, you can almost certainly save money by bundling these policies together with a single provider. Contact each of your current insurers individually, as well as several other competitors, to find the best bundling rate in your case. Bundling doesn’t guarantee savings every single time, so check out competitors’ rates for individual policies as well.

Use public transportation instead of driving.

Public transit is good for the environment and usually your wallet. Add up how much you spend each month on fuel, parking, and upkeep for your vehicle, then compare that to public transportation costs. In nearly all cases you’ll save quite a bit by using the second option. The savings can be especially large if you commute to work or school in a densely populated area. Depending on how close you live to your workplace or school, biking or walking might be another alternative to driving. You may even be able to sell your vehicle and put some extra money in your pocket.

Carpool to work if driving is necessary.

Split up the cost of your commute with one or more coworkers. Public transportation isn’t always an option, but carpooling is often a viable alternative to driving yourself to work (or school) every day. Ask coworkers who live nearby about starting a carpool schedule. Take turns driving to work to save 50% or more on your fuel, parking, and vehicle upkeep expenses. Alternatively, instead of taking turns driving, have a single driver (with a reliable vehicle) and have all the passengers “chip in” a fair share of the cost.

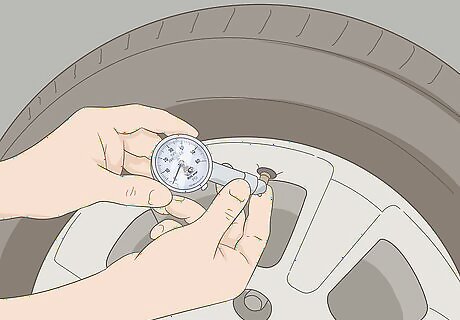

Keep your tires and vehicle well-maintained.

Simple steps like checking your tire pressure can have big savings. Keeping up with routine maintenance measures can have a real impact on your vehicle’s fuel efficiency—and therefore your pocketbook. Consider the following potential savings: Proper tire pressure: 2 cents (USD) per 1 US gal (3.8 L). Routine tuneups: 13 cents per gallon. Use of proper motor oil: 3-6 cents per gallon. If you use 10 US gal (38 L) of fuel per week at $3 USD per gallon, these measures can save you over $100 USD per year.

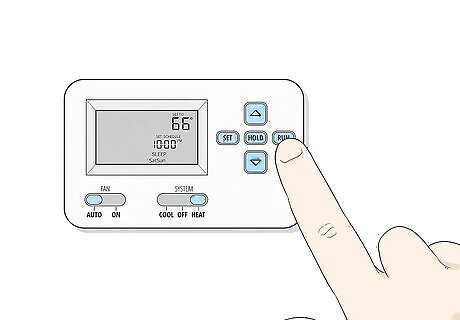

Adjust your thermostat to reduce heating/cooling costs.

Aim for general comfort when you’re home, not perfect comfort always. For example, adjust your thermostat down a few degrees in winter, put on a sweater, put it up a few degrees in summer, and set up a fan. When you’re out of the house, turn your thermostat to 65 °F (18 °C) in the winter and 80 °F (27 °C) in the summer, or invest in a smart thermostat that automatically adjusts. Consider investing in ceiling fans. They can dramatically reduce the cost of heating and cooling by circulating the air more efficiently. When the weather isn’t too hot, turn off your A/C and rely on open windows and fans to keep cool.

Use energy-efficient light bulbs and appliances.

Choose products with the “Energy Star” rating in the United States. The simple act of replacing incandescent bulbs with LED bulbs can save you around $50 USD in annual energy costs. Replacing all your lighting and appliances with energy-efficient models may be able to save you 25% in total energy costs. That can easily add up to several hundred U.S. dollars per year! Many countries have programs similar to the Energy Star program in the U.S. Energy Star-rated items often cost more upfront, but they use energy more efficiently and will save you money in the long run. In some cases, it may make more economic sense to replace all your appliances at once and maximize your energy cost savings. Other times, it’s better to replace items one at a time as needed. It all depends on factors like your current budget and current energy usage costs.

Unplug your electronics when you aren’t using them.

Reducing “vampire loads” can save you $100 USD per year. Even when your electronic devices are turned off, they are still using energy if they are plugged in. This wasted electricity is known as a “vampire load.” If unplugging things like your TV is a hassle, buy smart power strips that automatically cut the power when the device isn’t being used. Unplugging your devices also gives you protection from power surges.

Take shorter, cooler showers.

Install a reduced flow shower head to further boost your savings. Taking a 10-minute shower with a standard showerhead uses about 20 US gal (76 L) of water. By cutting your shower time in half, reducing the temperature a few degrees, and using a water-smart shower head, you can cut your water and energy usage (and water and energy bills) substantially. Speed up your shower by using fewer products and soaping up right away once you step in. Set a timer on your phone to remind you when your time is up. By taking more water- and energy-efficient showers, an average family of 4 can, in 1 year, save the amount of electricity used to power a TV for 1 ½ years.

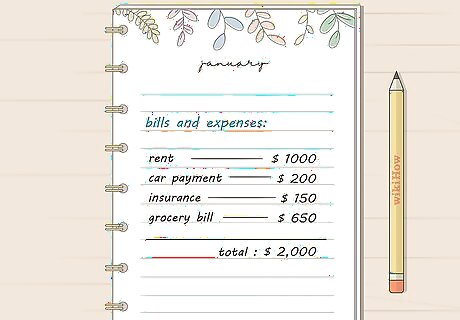

Analyze your spending.

Track your expenses for a month to find additional potential cuts. Record all your recurring expenses, like your monthly mortgage or rent, car payment, and insurance payment, as well as your average weekly grocery bill. Also keep track of every time you spend money, no matter how small the amount. Keep a note on your phone or paper and write down each expenditure. Group your notes by category—dining, entertainment, transportation, etc.—to make it easier to analyze where your money is going each month. Once you have a record of your monthly expenses, review what you are actually spending money on and then decide what you can cut back on.

Make a monthly budget you can stick to.

Lay out your spending plan and hold yourself accountable to it. Use your spending analysis and the cuts you’ve identified to lay out a realistic but aggressive monthly budget—cutting back by 20% may be manageable, for instance, while 60% probably isn’t. Set up a reward for yourself at the end of the month—such as a nice (but not completely budget-busting) dinner out—if you hold to your budget. Try using the following worksheet to lay out your budget: https://www.consumer.gov/content/make-budget-worksheet One way to lay out a budget is to use the 50/30/20 rule: dedicate 50% of your income to necessities, 30% to wants, and 20% to savings (or paying down debt).

Sell stuff you don’t need to make some money.

This may not reduce expenses, but it will help balance your budget. Unless you’re selling something like a car that carries lots of ongoing expenses, this option is less about cutting back and more about adding a bit more income. Go through your stuff and pick out things like clothes, books, movies, electronics, housewares, and collectibles that you can part with. Sell them online through sites like eBay, or hold an old-fashioned yard sale!

Comments

0 comment